The Yield Floor: What Collapsing DeFi Stablecoin Rates Are Really Telling You

Supply APYs have hit their lowest level since June 2023. Most observers see a bear signal. The smart money sees a setup for continued stablecoin adoption.

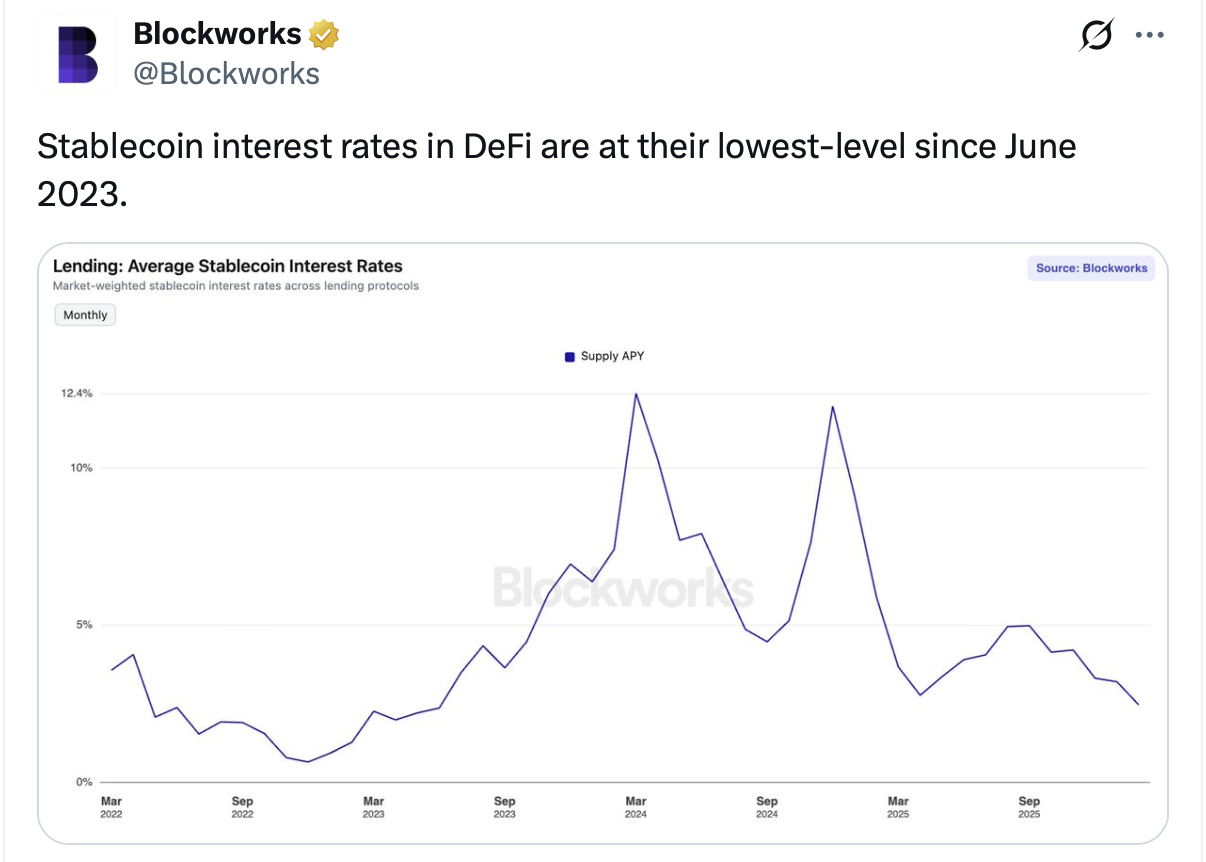

A chart making the rounds this week tells a stark story. According to Blockworks, the market-weighted average supply APY for stablecoins across major DeFi lending protocols has fallen to approximately 1.5% as of early March 2026—the lowest reading since June 2023. For context, those same rates peaked above 12% in early 2024 and flirted with 11% again in late 2024 before the slow bleed began.

The replies are predictable: bear market confirmed, DeFi is dead, nobody wants yield anymore. But, that narrative is wrong—or more precisely—it is asking the wrong question.

The right question is not why yields are low. The right question is what that compression means for where we are in the cycle, and how you should be positioned when the tide turns.

Low yield isn’t a death sentence for DeFi. It’s the accumulation phase. The people who understand the ecosystem now, at the boring moment, are the ones who capture the upside when rates rip back.

First, Understand What DeFi Yields Actually Measure

DeFi stablecoin supply rates are not set by a central bank. They are not administered. They are real-time, market-clearing prices for the cost of borrowing capital on-chain.

When traders are bullish, when they want leverage to go long ETH, BTC, or whatever narrative is running hot, they borrow stablecoins to do it. That borrowing demand drives up the utilization rate in lending pools like Aave. Higher utilization means higher rates for suppliers. You saw this mechanism fire in March 2024 at the height of ETH futures mania, and again in November 2024 following post-election euphoria.

When traders go risk-off, when macro uncertainty spooks the market, when volatility collapses, when nobody wants to lever up, borrowing demand evaporates. Utilization falls. Rates compress. That is precisely where we are today.

So yes: 1.5% average supply APY is a signal of muted leveraged speculation. But conflating that with ‘stablecoins are failing’ is like looking at a slow week in crypto spot volume and concluding exchanges are shutting down.

The Supply Paradox Nobody Is Talking About

Here is the data point that should stop you cold: even as yields have cratered, total stablecoin supply has surged past $320 billion as of early March 2026, up from roughly $205 billion at the start of 2025. That is a greater-than-50% increase in stablecoin market capitalization during the same period yields were declining.

Let that sink in. Supply nearly doubled. Yields collapsed. And yet adoption accelerated.

In a purely financial instrument, that makes no sense. If yield is the only value proposition, capital should flee when yields drop. But it didn’t. It poured in. Why?

Because stablecoins stopped being just a yield product a long time ago. Stablecoins are becoming the infrastructure layer for cross-border settlement, payroll, treasury management, DeFi collateral, AI micro payments, and remittances. These use cases for stablecoins continue to gain market share regardless of drop in DeFi stablecoin lending rates.

Spend in stables. Stack in sats. Make your wallet your bank. The premise was never about chasing 12% APY. It was about taking back control of your financial life — and that thesis doesn’t expire when DeFi rates go quiet.

The GENIUS Act Wildcard and Why Low Rates May Ironically Accelerate DeFi

The regulatory backdrop adds a critical layer. The GENIUS Act, signed into law in July 2025, established the first federal framework for stablecoin issuance in the United States. Implementation is expected to begin in the spring of 2026, with full legal effect no later than early 2027.

Here is what most commentary gets wrong about the GENIUS Act and yield: the banking lobby’s sustained effort to strip yield-bearing provisions from regulated stablecoins will not kill stablecoin yield. It will route it through DeFi.

If federally-regulated stablecoin issuers are prohibited from passing yield to holders—a real possibility under lobbying pressure—consumers who want that yield will have exactly one place to go: permissionless, on-chain lending markets. The banks may win the regulatory battle and lose the economic war. Regulatory arbitrage has been DeFi’s greatest growth catalyst historically, and there is no reason to think 2026 will be different.

In short: low rates today, combined with restrictive regulation on CeFi yield products, is a coiled spring. The compression is creating the setup for the next expansion.

Reading the Historical Pattern: How Fast Can Rates Reverse?

Look at the Blockworks chart carefully. In mid-2023, supply APYs were near their floor—sub-2%, almost exactly where we are today. By March 2024, rates had surged past 12%. That reversal took roughly eight months.

The mechanism is reflexive and fast. One sustained BTC breakout. One macro catalyst—a Fed pivot, a major institutional announcement, a legislative tailwind—like passage of the CLARITY Act with a fair compromise on stablecoin rewards. Trader sentiment flips, leveraged positions open, utilization spikes, and rates reprice within days, not months. Anyone who waited for yields to ‘confirm’ the bull move before supplying liquidity in 2023 missed the majority of the return.

What This Means for the Self-Custody Thesis

My book, Make Your Wallet Your Bank, is built on a thesis that has nothing to do with any particular rate environment: the traditional banking system charges you rent to hold your own money. Fees, spread capture, float, and restrictions on access are the business model. You are not the customer. You are the product.

Stablecoins—held in self-custody, used for daily commerce, deployed strategically in DeFi—invert that model. You become the bank. You capture the yield that your custodian bank historically pocketed. You settle transactions without permission, without SWIFT delays, without wire cutoff times.

The 1.5% DeFi rate environment of March 2026 does not undermine that thesis. In fact, it clarifies it. Even at 1.5%, you are earning more on your dollar than a standard checking account pays. Even at 1.5%, your assets are not rehypothecated without your consent. Even at 1.5%, you have 24/7 access, global settlement finality, and no counterparty holding your funds hostage.

And if rates return to 8%, then every additional basis point accrues to you, not to a bank’s net interest margin.

The yield floor is not a ceiling on your potential. It is the quiet before the compounding begins.

The Bottom Line

The Blockworks chart showing DeFi stablecoin supply APYs at their lowest level since June 2023 is not an obituary. It is a trough marker—the kind that precedes reversals, not collapses.

The stablecoin market grew 50% in 2025 during a yield compression cycle because the utility story is now larger than the yield story. Regulatory clarity under the GENIUS Act is accelerating institutional adoption even as it may inadvertently turbocharge DeFi by restricting CeFi yield. And the historical pattern is unambiguous: this rate floor has preceded explosive yield expansions twice in three years.

If your strategy depends on a 12% APY to work, you are speculating. If your strategy is built on sovereignty, self-custody, and stablecoins as functional financial infrastructure—then the current rate environment is simply a quiet Tuesday, and you already own the right assets.

Spend in stables. Stack in sats. Make your wallet your bank.

The yield will catch up with the thesis. It always does.