The Banks and Elizabeth Warren's Anti-Crypto Army Are At It Again

Take a moment to watch this important video. The banks and the anti-crypto army are once again trying to change the Clarity Act and limit consumer options for how they custody and move their money. You joined the Stablecoin Solutions community to learn how to break away from the banks and their toll booth economy. It's now more important than ever that you learn how make your wallet your bank. Together, we can do this.

Transcript:

(00:00:00):

Elizabeth Warren and the Anti-Crypto Army are back at it again.

(00:00:05):

The Clarity Act,

(00:00:06):

which is the most significant piece of crypto legislation to have advanced this far

(00:00:10):

in Congress,

(00:00:12):

is set for a floor markup vote on Thursday,

(00:00:15):

May 14th.

(00:00:16):

In advance of that markup vote,

(00:00:18):

over 100 amendments have been proposed,

(00:00:21):

flooding the zone with a ton of anti-crypto,

(00:00:25):

anti-stablecoin,

(00:00:26):

and anti-DeFi legislation.

(00:00:29):

A lot of that coming from Elizabeth Warren herself.

(00:00:32):

They want to eliminate your ability to self custody your crypto.

(00:00:35):

They want to eliminate your ability to privately move your money how you want to

(00:00:39):

move your money.

(00:00:41):

And they want to create a surveillance state.

(00:00:43):

They want to eliminate crypto from the financial system based on what I'm reading

(00:00:47):

in these amendments.

(00:00:49):

I'm not surprised by any of this.

(00:00:51):

I've been talking lately about how the banks have been doing a full front assault

(00:00:56):

through their lobbying groups

(00:00:57):

on the stablecoin provisions of the Clarity Act.

(00:01:01):

The Clarity Act, just to be clear, is more than just stablecoin legislation.

(00:01:06):

This creates the regulatory and legal infrastructure for how digital assets

(00:01:11):

integrate with the banking and financial system in this country.

(00:01:15):

We previously chased this innovation overseas through overzealous regulation,

(00:01:21):

and that's why the Clarity Act is critically important to pass.

(00:01:25):

And all of this last-minute

(00:01:27):

Wrangling by the bank lobby,

(00:01:30):

who have flooded Congress with over 8,000 letters in opposition to the yield

(00:01:35):

provisions of the Clarity Act,

(00:01:37):

which would allow you as consumers to be able to earn interest on your stablecoins,

(00:01:41):

shows you just how desperate they are to shut all of this innovation down.

(00:01:46):

I've talked about this previously,

(00:01:47):

and in my book,

(00:01:49):

Make Your Wallet Your Bank,

(00:01:51):

I give you the roadmap for how to break away from the banks and their tollbooth

(00:01:54):

economy

(00:01:56):

Today might be a good day to download that free copy and learn how to make your

(00:02:00):

wallet your bank because it is clear based on what the banks are trying to do and

(00:02:05):

what Warren and her anti-crypto army are trying to do that they want to eliminate

(00:02:10):

those options for consumers.

(00:02:12):

Consumers deserve choices on how they custody and move their money and the best way

(00:02:17):

you can send a message to these legislators is to share this and make it viral.

(00:02:22):

Let them know that you want control over how you move and custody your money and

(00:02:27):

that you want to break away from the banks and their fee extraction monopoly.

(00:02:32):

This is all about protecting legacy financial rails and denying consumers the right

(00:02:38):

to have options.

(00:02:40):

And those options come in the form of cryptocurrencies and stablecoins that are

(00:02:44):

fully regulated on the Genius Act.

(00:02:47):

Enough is enough.

(00:02:49):

Let's get this bill marked up

(00:02:51):

Let's get it out of the Senate and let's get it to the White House and signed into

(00:02:54):

law because that's the right thing for consumers.

THE MONETARILY FREE: How to Escape the Bank, Move Money Anywhere, and Reclaim Your Financial Life

It’s 9:47 PM on a Tuesday in East Los Angeles. Maria is closing her taqueria, and she’s smiling.

This is unusual. Tuesday used to be the night she dreaded—the night the credit card processing statement always landed in her inbox, the night she watched another $300 evaporate into Visa, Mastercard, her processor, and the gateway fees nobody ever explained to her. For eleven years she ran the numbers in her head: 3.4% of every breakfast combo, every birria plate, every horchata. Eighteen thousand dollars a year. A second employee. A new walk-in. Her daughter’s tuition. Money that existed, money she earned, money that vanished into a four-layer fee structure she had no power to negotiate.

Tonight, none of that disappeared. When her last customer paid, the money landed in her wallet in 1.8 seconds. The fee was a fraction of a penny. The dining room she’s looking at—the four extra tables, the new lighting, the second deep fryer—was paid for with money she used to mail to a payment processor in Atlanta.

Maria didn’t get richer. She just stopped getting poorer.

And she’s not the only one. There’s a quiet exodus happening, and almost nobody is writing about it. People are walking out of the banking system the same way a previous generation walked out of cubicles—not in protest, not with manifestos, just leaving. They’re keeping more of what they earn. They’re sending money to their families in Lagos and Manila and Mexico City in seconds, not days, for pennies, not percentages. They’re earning yield on their own dollars instead of donating it to a bank’s quarterly earnings call.

I’m going to tell you how they did it. I’m going to tell you how you can do it. But first, you need to understand what you’re escaping from.

The Tollbooth Life

There is a default financial life in America, and almost everyone is living it. It looks like this:

You earn money. It lands in a checking account that pays you 0.07%—twenty-eight dollars a year on a $40,000 balance, while the bank lends those same dollars out at 8.5% and pockets $3,400. You pay $35 to send a wire. You pay $27 if your account dips $2 into the negative. You pay $4 to use the wrong ATM. You pay 2.9% every time you swipe to accept a customer’s payment. You wait three to five business days for your own money to clear. You pay $40 every time you send $500 home to your mother.

You are paying rent to access what’s already yours.

This isn’t a glitch. It’s the architecture. Every fee, every delay, every two-day hold on a direct deposit that could clear in milliseconds—none of it is an accident. The system was designed by and for the institutions that profit from it, refined over decades to extract just slightly less than the threshold at which you’d leave. The six largest U.S. banks made over $140 billion in profit last year. JPMorgan Chase alone made $58.5 billion. A meaningful percentage of that came from people like you, doing nothing, sitting still, earning 0.07% while their purchasing power eroded by another 3% to inflation.

This is the Tollbooth Life. You don’t have to drive on the toll road. You just can’t get to work without it. Until now.

Meet the Monetarily Free

The escape isn’t theoretical. Real people are doing it. Not Silicon Valley billionaires. Not crypto bros. Plumbers. Restaurant owners. Freelance designers. Mothers sending money home. Let me introduce you to a few.

Maria, 47, taqueria owner, East Los Angeles

Eleven years in business. Six employees. The best birria in the neighborhood. Used to lose $16,320 a year to credit card processing—a 3.4% blended rate she had no power to negotiate. As her customers shifted to stablecoin payments, she started reclaiming it. A QR code at the register. Settlement in 1.8 seconds. Fees that round to zero. She didn’t get a raise. She gave herself one.

Aisha, 34, medical billing specialist, Houston

Every month for years, she sent $500 to her mother in Lagos through Western Union. Every month, $40 disappeared into the remittance machine. Over a decade, that’s $4,800—money that should have bought medicine, paid school fees, fed her family. She switched. The money now lands in her mother’s wallet in minutes for under a dollar. The 8% remittance tax that working families in this country have been paying for forty years? Aisha doesn’t pay it anymore.

Derek, 52, plumber, Columbus, Ohio

$40,000 in a checking account at a national bank, earning $28 a year. The bank lends it out at 8.5% and earns $3,400 on the spread. He kept it there because his father did. His father before him. Then he ran the math—really ran it—and realized he was the cheapest source of capital in the entire financial system, and he didn’t even know it. He started moving a portion into stablecoins he holds himself. He stopped donating his savings to a bank’s balance sheet.

Sandra, 39, jewelry maker, Brooklyn

Sells handmade earrings online. The platform takes 6.5% in fees and then—here’s the part nobody talks about—holds her money for three to five business days. During that week, her capital is trapped in someone else’s system, earning interest for someone else, while she waits. With direct stablecoin payments, settlement is instant. The customer pays. The money’s hers. She buys materials that afternoon. The cost of delay disappears.

Ray, 58, landscaping company owner, Atlanta

$185,000 in his business checking account. Twenty-two employees. One Thursday morning his account was frozen with no warning, no phone call, no explanation. Three weeks later it was released, also with no explanation. By then he’d lost two employees, a $30,000 contract, and roughly $60,000 in damages. The bank faced zero consequences—because buried in the agreement he signed years earlier was a clause giving them the right to do exactly that. For any reason. With or without notice. Ray now keeps his operating capital in a wallet he controls. Nobody can freeze it on a Thursday morning because they don’t like his cash deposits.

Six different lives. Six different occupations. One pattern. They all looked at the system, ran the numbers, and concluded the same thing:

The bank was charging them rent on their own money—and there was finally somewhere else to live.

The New Framework: Spend in Stables. Stack in Sats.

Every system of personal liberation needs a framework. A way to think. A way to act. The framework that lets ordinary people opt out of the Tollbooth Life is one sentence long, and once you understand it you can’t unsee it:

Spend in stables. Stack in sats. Make your wallet your bank.

Translate that out of jargon and here’s what it actually means.

Spend in stables

A stablecoin is a digital dollar. One token equals one US dollar, backed one-to-one by reserves, regulated under the GENIUS Act. It moves at the speed of email. It settles in seconds, 24 hours a day, 365 days a year. It costs a fraction of a penny to send. It doesn’t care if it’s 3 AM on Christmas Eve or 4:58 PM on a Friday before a holiday weekend.

This is your operating system. This is how you accept payments, send invoices, pay vendors, send money home. This is the layer that replaces Visa, Western Union, ACH, and the wire desk at your bank.

Stack in sats

A sat is a Satoshi—one one-hundred-millionth of a Bitcoin. Bitcoin has a fixed supply of 21 million. No government can print more. No central bank can dilute it. No emergency, no pandemic, no election can change the math. The dollar in your pocket has lost 96% of its purchasing power since 1913. Bitcoin is the exit from that trajectory.

This is your vault. This is the long-term store of value. You don’t need to buy a whole one—you stack sats consistently, the way previous generations dollar-cost averaged into index funds. You’re betting that 21 million is a smaller number than infinity. The math is on your side.

Make your wallet your bank

A wallet is the thing your grandmother carries. It holds your money, in your possession, under your control. A bank is also a container for your money—but it’s someone else’s container, with someone else’s rules, someone else’s fees, and someone else’s power to lock you out.

The entire thesis is replacing one container with another. The technology now exists to do everything a bank does—hold money, move money, earn on money—without a bank.

The Six Rules of Monetary Freedom

Frameworks are useful. Rules are operational. These are the six I’d give a friend over coffee if they asked me where to start. Print them out. Tape them to the wall. Argue with them. Then live them.

1. Stop confusing safe with sovereign. Your bank account is safe from bank failure. It is not safe from inflation, debanking, account freezes, two-day holds, or the slow erosion of what your money can buy. Safe and sovereign are not the same word. The Tollbooth Life optimizes for the first and ignores the second. The Monetarily Free optimize for both.

2. Audit your tollbooths. Pull your last three months of bank and processor statements. Add up every fee. Every overdraft, every wire, every monthly maintenance, every foreign transaction, every percentage point on every card swipe. Most people have never done this in their entire lives. The number will shock you. The number is your raise.

3. Separate your spending layer from your savings layer. Stables for spending. Sats for saving. They do different jobs. Stables are stable on purpose—one dollar today, one dollar tomorrow, predictable enough to run a business. Sats are volatile on purpose—because scarcity is the whole point. Mix them up and you’ll panic-sell the savings layer to cover next week’s rent. Keep them separate and the framework works.

4. Hold your own keys, eventually. Self-custody is the destination, not the starting line. If self-custody feels overwhelming today, start on a regulated exchange while you learn. Perfect is the enemy of good. The strategy matters more than the custody method. But know that as long as someone else holds the keys, someone else holds the power. Move toward sovereignty at the speed of your own comfort.

5. Move at the speed of your understanding. Never put money into something you can’t explain to a 12-year-old in two sentences. Never chase a yield you don’t understand. The platform graveyard is full of people who wired their savings to companies promising 18% returns and never asked how. If you can’t explain where the yield comes from, the answer is: from you.

6. Plan for the day after tomorrow. Self-custody means self-responsibility. If you hold your own keys and get hit by a bus, your family inherits nothing unless you’ve documented the path. An estimated 20% of all Bitcoin ever mined is permanently lost—because nobody planned. Write the plan. Tell one trusted person. Update it once a year. Sovereignty without succession is just a slow leak.

The Hidden Tax Nobody Lists on Your Statement

Here’s what most financial writing misses, and what the Monetarily Free understand at a cellular level:

The most expensive line item in your financial life is not on any statement.

It’s the inflation tax. Every dollar the Federal Reserve creates dilutes the value of the dollars you already hold. You don’t see it on a 1099. You don’t pay it on April 15th. There’s no line on your bank statement. But it’s there—every month, eating your savings alive. Derek’s $40,000 earns $28 a year in interest while inflation quietly eats $1,200. He’s losing forty-three times what he’s earning, and the bank statement won’t mention it.

The Monetarily Free aren’t paranoid about inflation. They’re realistic about it. They hold a portion of their wealth in something that cannot be diluted by anyone, anywhere, ever—because over a long enough timeline, that’s the only protection there is.

The Life You’re Building: Picture a Tuesday a year from now.

Maria closes her taqueria at 9:47 PM. She’s not paying $50 in processing fees on the day’s sales. She’s looking at the second deep fryer she bought with the savings.

Aisha sends $500 to her mother in Lagos from her phone while watching Netflix. The money arrives before the next commercial break. The fee is less than a dollar.

Derek pays a supplier from his truck at a job site. The payment settles before he’s back in the cab. His operating capital is no longer subsidizing a bank’s auto loan portfolio.

Sandra ships an order to Tokyo. The customer pays in stablecoins. The funds are in her wallet before she’s printed the shipping label. She buys silver wire that afternoon.

Ray runs payroll on a Thursday morning. Nobody can freeze his account because nobody owns it but him.

None of them are rich. None of them quit their day jobs. None of them moved to a beach in Bali. They just stopped paying rent on their own money. They just made their wallet their bank.

And that, more than any single asset or any single technology, is what monetary freedom actually looks like. Not a windfall. Not a lottery ticket. Not a single dramatic move. A series of small, deliberate decisions that compound—quietly, patiently, over years—into a financial life that belongs to you instead of to an institution.

The tools exist. The legal framework is in place. The on-ramps are open. The only question left is whether you’re going to keep paying tolls on a road you didn’t ask to be on, or whether you’re going to take the exit that’s been there all along.

Spend in stables. Stack in sats. Make your wallet your bank.

Welcome to the Monetarily Free.

IMPORTANT DISCLAIMER

Not Financial, Legal, Investment, or Tax Advice. This article is provided for educational and informational purposes only. Nothing contained in this article constitutes—or should be construed as—legal advice, financial advice, investment advice, tax advice, accounting advice, or a recommendation to buy, sell, hold, or transact in any cryptocurrency, stablecoin, digital asset, security, or other financial instrument. The author, Carlo D’Angelo, is a licensed attorney but is not acting as your attorney through this publication, and no attorney-client relationship is created by reading this article. The author is not a registered investment adviser, broker-dealer, financial planner, certified public accountant, or tax professional.

Substantial Risk of Loss. Cryptocurrency, stablecoins, Bitcoin, and digital assets involve substantial risk, including the potential loss of your entire investment. Digital asset prices can be extraordinarily volatile and may fluctuate dramatically in short periods. Past performance is not indicative of and does not guarantee future results. Stablecoins, while designed to maintain a one-to-one peg with the U.S. dollar, may lose their peg, become illiquid, or fail entirely—as has occurred multiple times in the history of the asset class. The strategies and case studies described in this article are illustrative and may not reflect actual results. Fee savings figures are approximations based on publicly available data and assume conditions that may not apply to your specific circumstances.

Self-Custody Risks. Self-custody of digital assets carries unique and serious risks, including but not limited to: permanent and irrecoverable loss of funds due to lost, stolen, or compromised private keys or seed phrases; smart contract vulnerabilities or exploits; phishing, malware, and social engineering attacks; user error in sending transactions to incorrect addresses; theft; hardware failure; and technical failures of underlying blockchain networks. There is no FDIC insurance, SIPC protection, or government-backed guarantee for self-custodied digital assets. There is no customer service hotline to reverse a mistaken transaction. Once digital assets are sent or lost, recovery is generally impossible.

Counterparty and Platform Risk. Holding stablecoins, Bitcoin, or any digital asset on an exchange, custodian, lending platform, or other third-party service exposes you to counterparty risk, including the risk of platform insolvency, fraud, hacking, regulatory action, freezes, and total loss of funds. The collapses of FTX, Celsius, BlockFi, Voyager, and others demonstrate that even seemingly reputable platforms can fail catastrophically with little warning. Decentralized finance (DeFi) protocols carry additional risks including smart contract bugs, governance attacks, oracle failures, and liquidation risk.

Regulatory Uncertainty. The legal and regulatory landscape for cryptocurrency and digital assets is complex, evolving rapidly, and varies significantly by jurisdiction. Laws, regulations, tax treatment, reporting obligations, and compliance requirements may change at any time and may have changed since this article was written. Activities that are legal today may become illegal tomorrow. The application of existing laws to digital assets is in many cases unsettled. You are solely responsible for understanding and complying with all applicable laws and regulations in your jurisdiction.

Tax Obligations. Cryptocurrency and digital asset transactions may trigger taxable events, including income tax, capital gains tax, and reporting obligations. Tax treatment is complex and varies by jurisdiction, transaction type, and individual circumstances. You are responsible for accurately tracking, reporting, and paying any taxes owed on your digital asset activity. Consult a qualified tax professional before engaging in any cryptocurrency transactions.

Consult Qualified Professionals. Before making any financial, investment, legal, or tax decisions based on the information in this article, you should consult with qualified, licensed professionals—including a financial advisor, attorney, certified public accountant, and tax professional—who can evaluate your specific circumstances, risk tolerance, financial situation, and goals. Do not rely on this article as a substitute for personalized professional advice.

Your Sole Responsibility. By reading this article, you acknowledge and agree that you are solely responsible for your own financial decisions and that you will conduct your own independent research and due diligence before taking any action. The author, publisher, Stablecoin Strategies, Inc., d/b/a Stablecoin Solutions, and any affiliated parties expressly disclaim any and all liability for any losses, damages, costs, or expenses—direct, indirect, incidental, consequential, or otherwise—arising out of or in connection with your use of, reliance on, or actions taken based on the information presented in this article. The case studies, examples, and scenarios are illustrative and intended to demonstrate concepts; they do not represent guaranteed outcomes and your individual experience may differ materially.

Forward-Looking Statements. Statements in this article regarding the future of money, banking, monetary policy, regulation, or technology are forward-looking and reflect the author’s opinions and observations based on information available at the time of writing. They are not predictions, guarantees, or assurances of any future outcome. Actual events may differ materially.

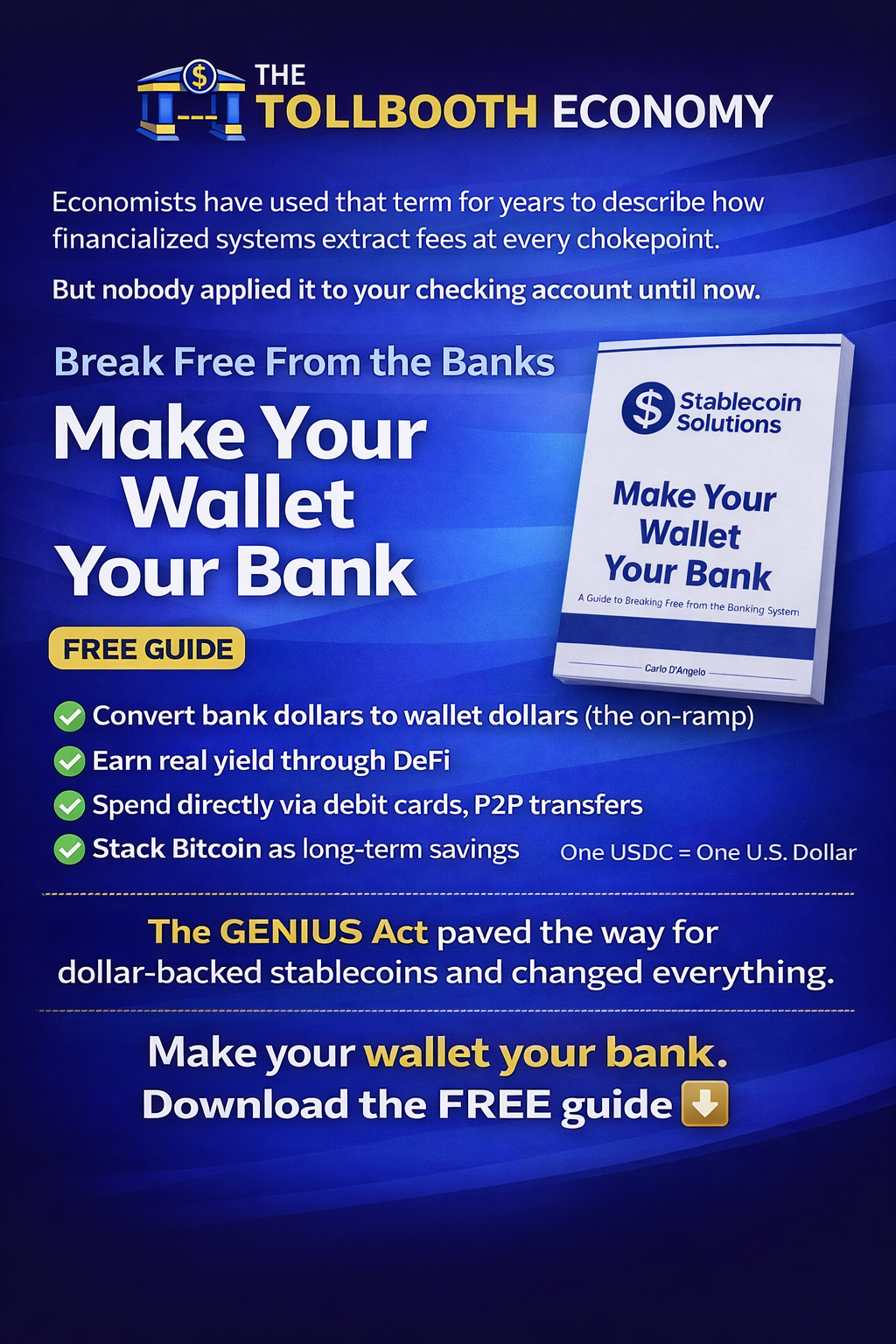

Stablecoins Offer An Alternative to the Tollbooth Economy

The Toolboth Econmy:

Economists have used that term for years to describe how financialized systems extract fees at every chokepoint. But here’s what they left out: the tollbooth isn’t just on Wall Street. It’s sitting right inside your checking account, skimming from your paycheck before you ever see it. Because that’s exactly what’s happening every time your paycheck lands at a bank. Your bank pays you 0.07% on deposits while lending your money out at 7%… 8%… 20%+ on credit cards. Wire fees. Overdraft fees. Foreign transaction fees. Monthly maintenance fees. You’re paying rent to access your own money.

Your dollars sit in their ledger. On their terms. Under their control.

The tollbooth isn’t on the highway. It’s in your wallet.

Here’s what changed.

The GENIUS Act just gave stablecoins—digital dollars that live in wallets you control—a soon-to-be fully federally regulated framework. For the first time in history, this isn’t a fringe experiment. It’s a recognized, regulated financial instrument with a legal foundation strong enough for consumers and small businesses to build on.

Once the GENIUS Act regulatory framework goes live, one USDC will be required under law to equal one U.S. dollar. No volatility. No 10% overnight swings. Just a dollar—except it lives in your wallet, not the bank’s database.

No bank can delay it. No bank can charge you rent to hold it. And, no bank can charge you outrageous fees to move it. Your money. In your wallet. And free to move on your terms.

Here’s the framework I lay out in Make Your Wallet Your Bank:

➡️ Convert bank dollars to wallet dollars (the on-ramp)

➡️ If you choose to, earn yield on those digital dollars through DeFi or on centralized crypto exchanges—the same type of yield banks pocket while paying you nothing

➡️ Spend directly via stablecoin-linked debit cards, merchant integrations, P2P transfers that settle in seconds

➡️ If you choose to, take the savings you earn on holding stablecoins and stack Bitcoin as your long-term savings layer—scarce, appreciating, outside the system entirely

Spend in stables. Stack in sats. Make your wallet your bank.

Here’s an excerpt from my new book that explains how banks take your money in the the tollbooth economy and how you can take back power and control over your money.

Where You Are Now: The Tollbooth Model

Think of your financial life today as a series of tollbooths. You earn money, it lands in a bank account, and from that moment forward, every time your money moves or sits still, someone is skimming a little off the top. Your checking account pays you essentially nothing while the bank lends your deposits out at 7%, 8%, 20%+ on credit cards. You pay wire fees, overdraft fees, foreign transaction fees, monthly maintenance fees. You’re paying rent to access your own money. That’s the core problem this book identifies.

Your money sits in one place (the bank), your investments sit somewhere else (a brokerage), your payments go through another set of rails (Visa, Mastercard, ACH), and every layer takes a cut. You don’t control any of it. If the bank decides to freeze your account on a Friday afternoon, you’re stuck until Monday—or longer.

The Bridge: What Stablecoins Actually Are

A stablecoin is just a digital dollar. One USDC (the largest U.S. based stablecoin in circulation) equals one US dollar. It’s not volatile like Bitcoin. It doesn’t swing 10% overnight. It’s a dollar that lives on a blockchain instead of in a bank’s ledger.

The key difference is where that dollar sits. In the traditional model, your dollar sits in a bank’s database, and the bank decides what you can do with it. With a stablecoin, your dollar sits in a wallet that you control with your own private keys. Nobody can freeze it, delay it, or charge you a monthly fee to hold it.

The Transition

The move from bank dollars to wallet dollars happens in stages. You start with the on-ramp—converting some of your traditional bank dollars to stablecoins through an exchange or on-ramp service. Think of it like exchanging currency at the airport, except you’re exchanging “bank dollars” for “wallet dollars.” Your purchasing power doesn’t change. A dollar is still a dollar. But now it’s in your possession rather than the bank’s.

From there, your stablecoins live in a digital wallet—an app on your phone, a hardware device, or a browser extension. The wallet doesn’t hold your money the way a bank does. It holds your keys—the cryptographic proof that those dollars belong to you. This is what the title of this book means: your wallet literally becomes your bank.

Once your dollars are in your wallet, you can lend them through decentralized finance (DeFi) protocols—automated, transparent lending platforms—and earn meaningfully more than the 0.07% your savings account pays. The yields come from the same place bank profits come from (people borrowing money), but without the bank sitting in the middle keeping the spread. You can spend stablecoins directly through debit cards linked to crypto wallets, merchant integrations, and peer-to-peer transfers that settle in seconds instead of days.

And once you’ve moved your day-to-day financial life onto rails you control, you allocate a portion into Bitcoin as a long-term store of value. The stablecoins handle your spending and short-term needs—stable, predictable, one dollar equals one dollar—while Bitcoin serves as your savings layer: scarce, appreciating over time, outside the traditional system entirely.

The Big Picture Shift

What this book describes is a change in who’s in charge. Today, banks are the gatekeepers—they hold your money, they set the terms, they extract fees, and they earn the yield on your deposits while paying you next to nothing. In the model I’m laying out, you become your own bank. Your wallet holds your dollars. You decide where to lend them and what yield to earn. You decide when and how to spend. Nobody charges you rent to hold what’s already yours.

The GENIUS Act and the regulatory framework around it is what makes this transition viable at scale—it gives stablecoins a legal foundation so that this isn’t some fringe experiment, it’s a recognized, regulated financial instrument.

That’s the thesis. That’s the framework. The rest of this book gives you the evidence, the tools, and the honest trade-offs you need to decide for yourself whether this path makes sense for you.

Spend in stables. Stack in sats. Make your wallet your bank.

Here’s a link to download your free copy today and join the community of people who are making their wallet their bank.

https://stablecoinsolutions.kit.com/39fe91a33e

IMPORTANT DISCLAIMER

This book is provided for educational and informational purposes only and does not constitute legal, financial, investment, or tax advice. The author, Carlo D’Angelo, is a licensed attorney but is not acting as your attorney, financial advisor, investment advisor, or tax professional through this publication. Cryptocurrency and digital assets involve substantial risk, including the potential loss of your entire investment. The value of Bitcoin, stablecoins, and other digital assets can fluctuate dramatically. Past performance is not indicative of future results. The regulatory landscape for digital assets is evolving rapidly, and laws described in this book may have changed since publication.

Nothing in this book should be construed as a recommendation to buy, sell, or hold any particular cryptocurrency, stablecoin, or digital asset. Before making any financial decisions, you should consult with qualified professionals including a licensed financial advisor, tax professional, and attorney who can evaluate your specific circumstances. The examples, scenarios, and case studies presented in this book are illustrative and may not reflect actual results. Fee savings estimates and cost comparisons are approximations based on publicly available data at the time of writing and may not represent your actual experience.

Self-custody of digital assets carries unique risks including but not limited to: permanent loss of funds due to lost or compromised private keys, smart contract vulnerabilities, user error, theft, regulatory action, and technical failures. The author assumes no liability for any losses incurred as a result of following the information presented in this book. By reading this book, you acknowledge that you are solely responsible for your own financial decisions and that you will conduct your own research and due diligence before taking any action based on the information contained herein.

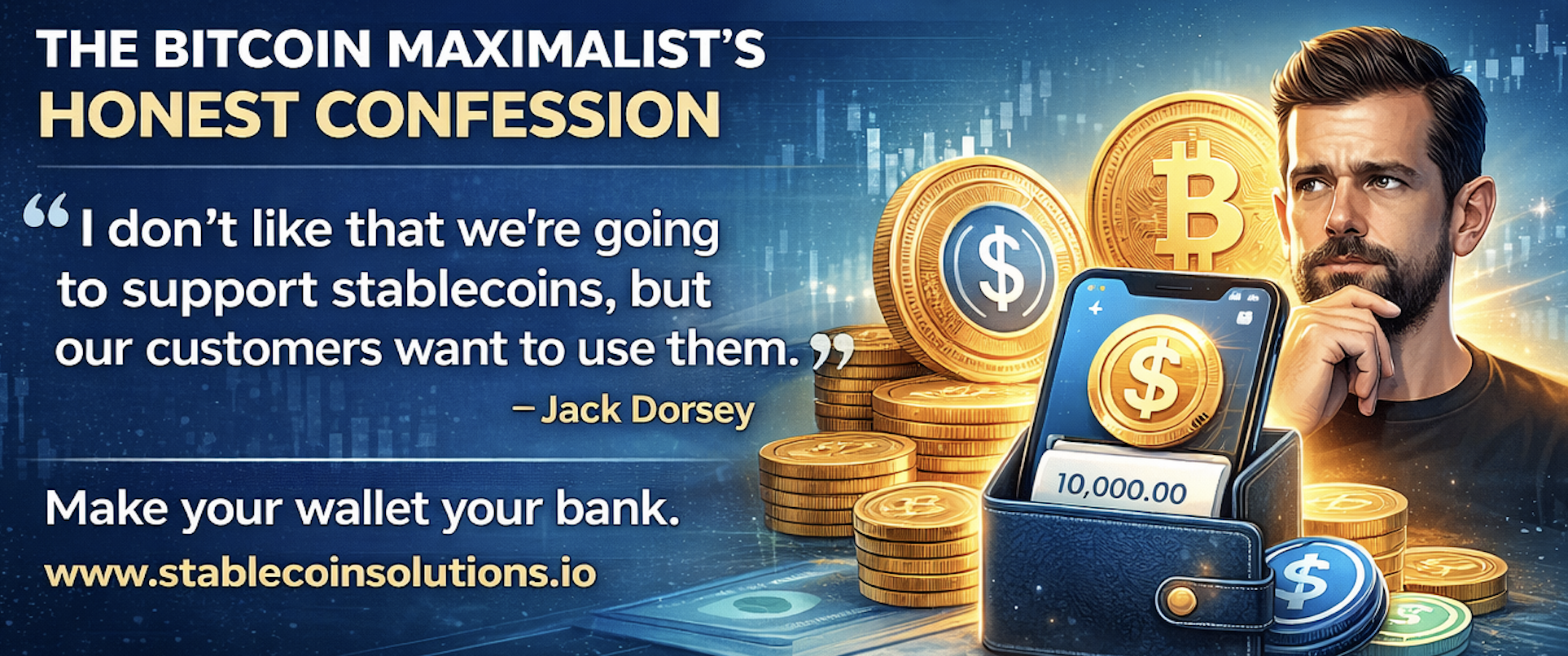

The Most Famous Bitcoin Maximalist on Earth Just Proved My Point

When the world's most famous Bitcoin maximalist pivots to stablecoins at the point of sale, the two-asset strategy stops being a theory and becomes a fact.

Jack Dorsey doesn’t like stablecoins. He’s said so publicly, repeatedly, and with the kind of conviction that only a true believer can muster. This is the man who once said that if he weren’t working on other projects, he would devote himself entirely to Bitcoin. The man who compared the Bitcoin white paper to poetry. The man who, when Facebook came calling about its Libra stablecoin project in 2019, the then-CEO of Twitter responded with two words: “Hell no.”

So when Dorsey recently announced that Block—his payments company, formerly Square—will be adding stablecoin support, the headline practically wrote itself. But for readers of this newsletter, the more important question isn’t what Dorsey said. It’s why the market forced him to say it.

And the answer validates everything I discussed in my new book, Make Your Wallet Your Bank.

The Bitcoin Maximalist’s Honest Confession

Here is Dorsey’s quote, and it deserves to sit alone for a moment:

“I don’t like that we’re going to support stablecoins, but our customers want to use them.”

Strip away the corporate framing and you have a world-class payments operator telling you, in plain English, that Bitcoin cannot yet function alone as a payment layer at the merchant point of sale. Not for his customers. Not at scale. Not right now.

This isn’t a minor footnote. Block built its crypto strategy entirely around Bitcoin. The company integrated BTC buying and selling through Cash App starting in 2017. It funded Bitcoin and Lightning Network developers. It launched hardware wallets and modular mining rigs. It accumulated 8,888 BTC—currently worth north of $600 million—on its corporate balance sheet. If any company on earth was positioned to prove that Bitcoin-only works at the consumer payment layer, it was Block.

And Block just blinked.

What Bitcoin Gets Right (And What It Can’t Do Alone)

Let me be precise here, because this isn’t a Bitcoin hit piece. I love Bitcoin! The case for Bitcoin has never been stronger. As a store of value, as a hedge against currency debasement, as a long-term wealth preservation tool—Bitcoin is doing exactly what it was designed to do. Its fixed supply, its decentralization, its credible neutrality, these are features, not bugs, and they are why serious investors are stacking it for the long haul.

But here’s the problem Bitcoin maximalists keep running into at the checkout counter: the vast majority of merchants don’t accept it.

Not on Cash App. Not on Square terminals. Not at your grocery store, your landlord’s payment portal, or your insurance company’s billing system. The Lightning Network, for all its promise, has not achieved the merchant or consumer adoption necessary to function as a day-to-day spending layer. Bitcoin is digital gold—and gold, historically, is not what you hand the cashier.

Dorsey knows this. His customers told him. And rather than hold the ideological line at the cost of his business, he made the pragmatic call.

The Two-Asset Strategy Isn’t a Compromise. It’s the Architecture.

Make Your Wallet Your Bank is built on one core thesis: Spend in stables. Stack in sats. Make your wallet your bank.

The two-asset strategy isn’t a consolation prize for people who can’t fully commit to Bitcoin. It’s the correct architecture for the world we actually live in—not the world many wish we lived in.

Stablecoins solve the merchant adoption problem. A dollar-pegged stablecoin is a dollar, settled in seconds, on rails that don’t sleep on weekends or charge 2-3% interchange. That’s why Stripe, PayPal, and now Block are racing to integrate them. That’s why the stablecoin market has surged to $318 billion in total market capitalization. That’s why Cash App announced stablecoin support in November 2025, making them interoperable with customers’ existing USD cash balances.

The market isn’t waiting for merchant Bitcoin adoption to catch up. The market built a workaround—and that workaround is stablecoins.

Meanwhile, Bitcoin keeps doing what it does best: appreciating, preserving wealth, and protecting holders from the slow-motion debasement of fiat currencies. You hold your Bitcoin. You spend your stablecoins. These two functions are complementary, not competing.

The Gatekeeper Problem (And Why It Doesn’t Change the Math)

To his credit, Dorsey didn’t abandon his principles entirely. His concern about stablecoins is worth hearing: “I don’t think it’s wise to go from one gatekeeper to another.”

He’s not wrong about the risk. A dollar-pegged stablecoin is still a dollar controlled by someone—a reserve custodian, a regulated issuer, a government that can freeze your account or blacklist your wallet. The GENIUS Act is now the law of the land and it will bring stablecoins further into the regulatory perimeter. That’s a real trade-off, and serious people should think about it.

But Dorsey’s philosophical objection to stablecoins doesn’t change the commercial reality his own company just validated. Ideological purity doesn’t process payments. And for people living in fiat economies—paying rent, buying groceries, covering insurance premiums—the relevant question isn’t “is this optimally decentralized?” It’s “does this work?”

Stablecoins work. Bitcoin doesn’t yet, not at the point of sale, not at mass-market and not at scale. The two-asset strategy accounts for both.

What This Means for You

If the most committed Bitcoin company in the payments space just integrated stablecoins because the market demanded it, ask yourself what that tells you about where the puck is going.

Stripe built it. PayPal built it. Block built it. The GENIUS Act is moving it into reality. The architecture of the new financial system is not Bitcoin-or-stablecoins. It is Bitcoin and stablecoins—each doing what it does best, held together in a self-custodied wallet that you control.

That is exactly the wallet my book was written to help you build.

Jack Dorsey didn’t mean to confirm my thesis. But market reality has a way of forcing honest people to tell the truth.

Spend in stables. Stack in sats. Make your wallet your bank.

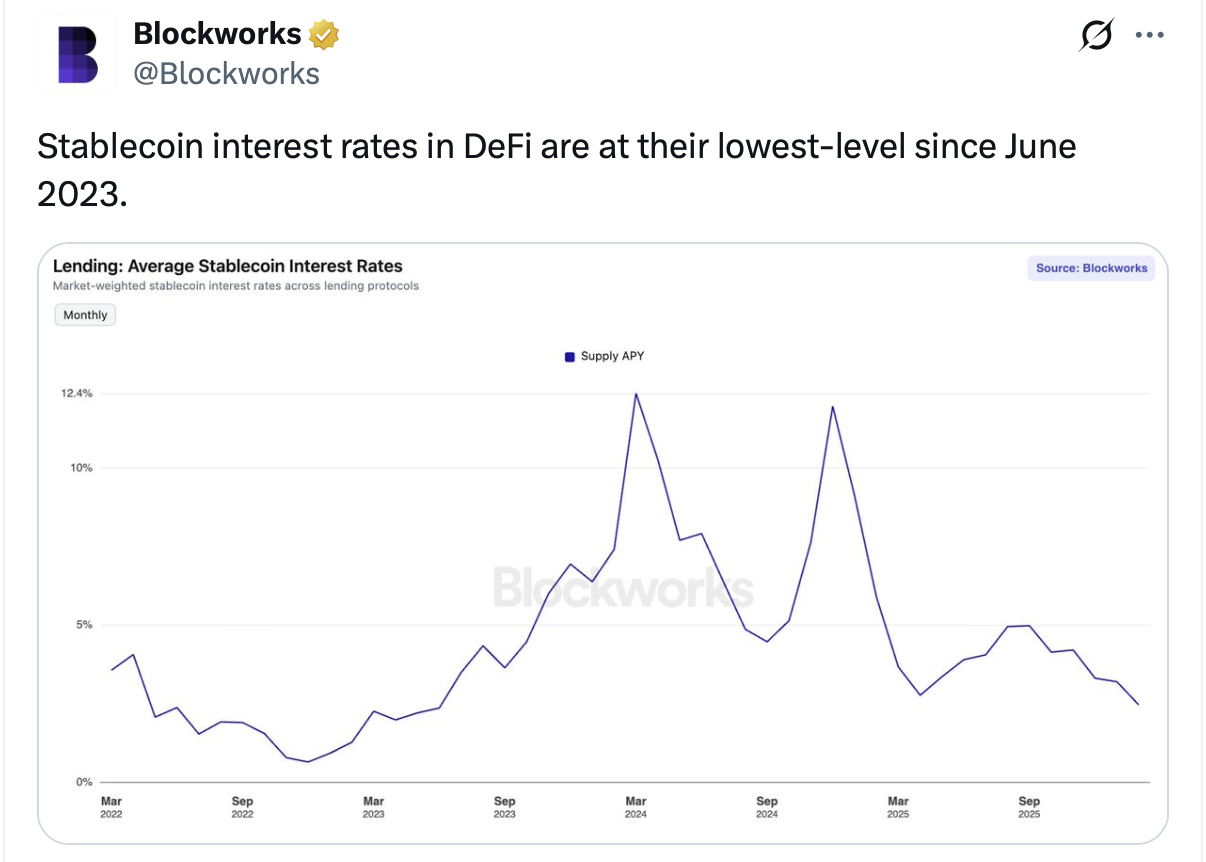

The Yield Floor: What Collapsing DeFi Stablecoin Rates Are Really Telling You

Supply APYs have hit their lowest level since June 2023. Most observers see a bear signal. The smart money sees a setup for continued stablecoin adoption.

A chart making the rounds this week tells a stark story. According to Blockworks, the market-weighted average supply APY for stablecoins across major DeFi lending protocols has fallen to approximately 1.5% as of early March 2026—the lowest reading since June 2023. For context, those same rates peaked above 12% in early 2024 and flirted with 11% again in late 2024 before the slow bleed began.

The replies are predictable: bear market confirmed, DeFi is dead, nobody wants yield anymore. But, that narrative is wrong—or more precisely—it is asking the wrong question.

The right question is not why yields are low. The right question is what that compression means for where we are in the cycle, and how you should be positioned when the tide turns.

Low yield isn’t a death sentence for DeFi. It’s the accumulation phase. The people who understand the ecosystem now, at the boring moment, are the ones who capture the upside when rates rip back.

First, Understand What DeFi Yields Actually Measure

DeFi stablecoin supply rates are not set by a central bank. They are not administered. They are real-time, market-clearing prices for the cost of borrowing capital on-chain.

When traders are bullish, when they want leverage to go long ETH, BTC, or whatever narrative is running hot, they borrow stablecoins to do it. That borrowing demand drives up the utilization rate in lending pools like Aave. Higher utilization means higher rates for suppliers. You saw this mechanism fire in March 2024 at the height of ETH futures mania, and again in November 2024 following post-election euphoria.

When traders go risk-off, when macro uncertainty spooks the market, when volatility collapses, when nobody wants to lever up, borrowing demand evaporates. Utilization falls. Rates compress. That is precisely where we are today.

So yes: 1.5% average supply APY is a signal of muted leveraged speculation. But conflating that with ‘stablecoins are failing’ is like looking at a slow week in crypto spot volume and concluding exchanges are shutting down.

The Supply Paradox Nobody Is Talking About

Here is the data point that should stop you cold: even as yields have cratered, total stablecoin supply has surged past $320 billion as of early March 2026, up from roughly $205 billion at the start of 2025. That is a greater-than-50% increase in stablecoin market capitalization during the same period yields were declining.

Let that sink in. Supply nearly doubled. Yields collapsed. And yet adoption accelerated.

In a purely financial instrument, that makes no sense. If yield is the only value proposition, capital should flee when yields drop. But it didn’t. It poured in. Why?

Because stablecoins stopped being just a yield product a long time ago. Stablecoins are becoming the infrastructure layer for cross-border settlement, payroll, treasury management, DeFi collateral, AI micro payments, and remittances. These use cases for stablecoins continue to gain market share regardless of drop in DeFi stablecoin lending rates.

Spend in stables. Stack in sats. Make your wallet your bank. The premise was never about chasing 12% APY. It was about taking back control of your financial life — and that thesis doesn’t expire when DeFi rates go quiet.

The GENIUS Act Wildcard and Why Low Rates May Ironically Accelerate DeFi

The regulatory backdrop adds a critical layer. The GENIUS Act, signed into law in July 2025, established the first federal framework for stablecoin issuance in the United States. Implementation is expected to begin in the spring of 2026, with full legal effect no later than early 2027.

Here is what most commentary gets wrong about the GENIUS Act and yield: the banking lobby’s sustained effort to strip yield-bearing provisions from regulated stablecoins will not kill stablecoin yield. It will route it through DeFi.

If federally-regulated stablecoin issuers are prohibited from passing yield to holders—a real possibility under lobbying pressure—consumers who want that yield will have exactly one place to go: permissionless, on-chain lending markets. The banks may win the regulatory battle and lose the economic war. Regulatory arbitrage has been DeFi’s greatest growth catalyst historically, and there is no reason to think 2026 will be different.

In short: low rates today, combined with restrictive regulation on CeFi yield products, is a coiled spring. The compression is creating the setup for the next expansion.

Reading the Historical Pattern: How Fast Can Rates Reverse?

Look at the Blockworks chart carefully. In mid-2023, supply APYs were near their floor—sub-2%, almost exactly where we are today. By March 2024, rates had surged past 12%. That reversal took roughly eight months.

The mechanism is reflexive and fast. One sustained BTC breakout. One macro catalyst—a Fed pivot, a major institutional announcement, a legislative tailwind—like passage of the CLARITY Act with a fair compromise on stablecoin rewards. Trader sentiment flips, leveraged positions open, utilization spikes, and rates reprice within days, not months. Anyone who waited for yields to ‘confirm’ the bull move before supplying liquidity in 2023 missed the majority of the return.

What This Means for the Self-Custody Thesis

My book, Make Your Wallet Your Bank, is built on a thesis that has nothing to do with any particular rate environment: the traditional banking system charges you rent to hold your own money. Fees, spread capture, float, and restrictions on access are the business model. You are not the customer. You are the product.

Stablecoins—held in self-custody, used for daily commerce, deployed strategically in DeFi—invert that model. You become the bank. You capture the yield that your custodian bank historically pocketed. You settle transactions without permission, without SWIFT delays, without wire cutoff times.

The 1.5% DeFi rate environment of March 2026 does not undermine that thesis. In fact, it clarifies it. Even at 1.5%, you are earning more on your dollar than a standard checking account pays. Even at 1.5%, your assets are not rehypothecated without your consent. Even at 1.5%, you have 24/7 access, global settlement finality, and no counterparty holding your funds hostage.

And if rates return to 8%, then every additional basis point accrues to you, not to a bank’s net interest margin.

The yield floor is not a ceiling on your potential. It is the quiet before the compounding begins.

The Bottom Line

The Blockworks chart showing DeFi stablecoin supply APYs at their lowest level since June 2023 is not an obituary. It is a trough marker—the kind that precedes reversals, not collapses.

The stablecoin market grew 50% in 2025 during a yield compression cycle because the utility story is now larger than the yield story. Regulatory clarity under the GENIUS Act is accelerating institutional adoption even as it may inadvertently turbocharge DeFi by restricting CeFi yield. And the historical pattern is unambiguous: this rate floor has preceded explosive yield expansions twice in three years.

If your strategy depends on a 12% APY to work, you are speculating. If your strategy is built on sovereignty, self-custody, and stablecoins as functional financial infrastructure—then the current rate environment is simply a quiet Tuesday, and you already own the right assets.

Spend in stables. Stack in sats. Make your wallet your bank.

The yield will catch up with the thesis. It always does.

The Fed Just Made It Official: Crypto Is Core Financial Infrastructure

Kraken Becomes the First Digital Asset Bank to Receive a Federal Reserve Master Account. The Banking Lobby Responded Within Hours. That Tells You Everything.

On March 4, 2026, Kraken Financial — the Wyoming-chartered banking arm of the Kraken exchange—was granted a Federal Reserve master account by the Federal Reserve Bank of Kansas City. That makes Kraken the first digital asset bank in U.S. history to receive direct access to the Federal Reserve's core payment infrastructure.

Let that sink in for a moment.

The same platform where millions of Americans buy Bitcoin and hold stablecoins can now settle transactions directly on Fedwire—the same payment rail the biggest banks in the country use. No intermediary. No correspondent bank. No middleman taking a cut and adding two business days to your money movement.

This isn't a press release milestone. This is a structural shift in American finance. And if you've been following the Make Your Wallet Your Bank thesis, you already know what comes next.

What a Fed Master Account Actually Means

Most people have never heard of a Federal Reserve master account, because most people have never needed to. It's the plumbing—the direct connection a financial institution gets to settle transactions across Fedwire, the backbone of the U.S. payments system.

Up until now, crypto exchanges had to route fiat through correspondent banks. That dependency created friction, cost, and a chokepoint the banking lobby was happy to maintain. Every wire, every ACH, every fiat on-ramp and off-ramp had to pass through a traditional bank that could—and sometimes did—close the account, slow the transaction, or simply decline to serve the client.

Kraken just cut that wire.

As Arjun Sethi, Co-CEO of Payward and Kraken, put it: “This milestone marks the convergence of crypto infrastructure and sovereign financial rails… we can operate not as a peripheral participant in the U.S. banking system, but as a directly connected financial institution.”

One important technical note: Kraken’s account is a limited-purpose, one-year account—sometimes referred to as a “skinny” master account—consistent with a framework the Federal Reserve has been developing for payments-focused, non-traditional financial institutions. It does not include interest on reserves, access to the Fed’s discount window, or the full suite of services available to traditional chartered banks. What it does include is something that has never before been granted to a digital asset institution: direct settlement on Fedwire. That is the historic part. And that is what the banking lobby immediately moved to attack.

The Banks Responded Within Hours. Read That Carefully.

Within hours of Wednesday’s announcement, three of the most powerful banking trade groups in Washington issued statements condemning the decision. Not days later. Not after deliberation. Within hours.

That is not the behavior of an industry that feels secure in its competitive position.

The Bank Policy Institute — which represents JPMorgan Chase, Bank of America, Wells Fargo, and Goldman Sachs—said it was “deeply concerned” that the approval came before the Federal Reserve finalized its policy framework, arguing that uninsured depository institutions present “substantially greater risks to the payment system.”

The Independent Community Bankers of America warned that the decision creates a two-tiered system in which crypto-focused institutions access payment rails without the same regulatory oversight applied to chartered banks.

The American Bankers Association’s Brooke Ybarra called it “another example of agencies taking significant action while the rules are still a work in progress,” adding: “This action puts the cart so far ahead, that the horse will never be able to catch up.”

There is a revealing subtext in all three statements. None of them argue that Kraken is technically unqualified. None point to a specific failure in Kraken’s operations or regulatory record. They argue about timing, process, and framework — the procedural tools of an industry that cannot win the substantive argument. When the banking lobby’s best counterargument is “the paperwork isn’t finished yet,” they have already conceded the field.

What they are really saying is this: if the Federal Reserve formalizes limited-purpose master accounts for payments-focused institutions, the competitive moat that has protected traditional banks for decades begins to drain. They are not wrong. That is precisely what is happening.

The cart is Kraken. The horse is the banks. If banks can’t catch up to the cart, then it’s because they continue to put profits over customers. When customers have options, they will chose the faster horse everytime.

Kraken Isn’t Just an Exchange Anymore — It’s a Better Bank

The banking lobby has spent years arguing that crypto exchanges are too risky, too unregulated, and too volatile to be trusted with real financial infrastructure. The Federal Reserve just disagreed—formally, and in writing.

But here’s what the banks don’t want you to notice: Kraken was already offering a better product.

Compare the security architecture of Kraken’s platform against what most traditional banks actually provide. The majority of legacy financial institutions still rely on username and password combinations fortified by SMS-based two-factor authentication—the same method security researchers have been warning against for years because of SIM-swap vulnerabilities. Though some larger banks are now finally in early-stages of adopting passkey adoption—finally! Traditional banks do not publish quarterly cryptographic proof that your deposits are actually there. They do not offer withdrawal address whitelisting with mandatory time-delay periods. And none of them have been operating under a full-reserve model that holds liquid assets equal to 100% of client deposits.

Kraken’s security stack includes:

• FIDO2-compliant passkeys with biometric authentication (fingerprint or Face ID), stored only on the user’s device — categorically resistant to phishing attacks

• No SMS or phone-based account recovery—deliberately engineered to eliminate SIM-swap attacks entirely

• Global Settings Lock (GSL) — a time-delay deadbolt that prevents any changes to account settings even if credentials are compromised

• Withdrawal address whitelisting with mandatory email confirmation and 72-hour delays for new addresses — meaning even a successful login cannot immediately drain funds to an unauthorized wallet

• Granular per-action 2FA — separate authentication required for login, trading, deposits, and withdrawals

• ISO/IEC 27001:2022 certification — the international gold standard for information security management

• Quarterly Merkle-tree Proof of Reserves audited by an independent accounting firm, with the September 2025 report confirming a 114.9% Bitcoin reserve ratio — meaning Kraken held more assets than it owed customers

https://theinvestorscentre.com/best-crypto-exchange/kraken-review/is-kraken-safe/

Kraken also carries a 13+ year track record with no customer funds ever lost to a security breach—an extraordinary record in a space where major competitors have suffered catastrophic failures. Its iOS App Store rating is 4.6/5 and 4.3/5 on Google Play. Users who complain do so about compliance friction and support response times—not about losing money.

Your bank publishes none of that. Because your bank cannot prove it.

This Is the First Domino, Not the Last

Kraken’s master account approval follows a deliberate, five-year regulatory engagement with the Federal Reserve and Wyoming supervisors. It was achieved through Kraken Financial’s status as a Wyoming Special Purpose Depository Institution (SPDI)—a full-reserve banking charter that requires liquid assets equal to or exceeding 100% of client deposits and strictly prohibits lending.

That’s right: Kraken Financial is legally required to operate more conservatively than most commercial banks, which borrow short to lend long and hold a fraction of deposits as reserves.

But make no mistake—Kraken won’t be alone for long. The moment regulators approved one digital asset institution for master account access, they created a blueprint every serious competitor will now follow. The trend line is clear: crypto exchanges are becoming neo-banks, and they are competing directly with the largest financial institutions in America for the everyday financial lives of consumers.

This matters enormously in the context of the GENIUS Act (which is law) and the CLARITY Act (which iscurrently moving through Congress). The banking lobby is simultaneously fighting Kraken’s Fed access and lobbying to eliminate stablecoin yield pathways at the centralized exchange layer. President Trump has already sided with the crypto industry on the stablecoin yield question, deepening the fault lines between legacy banking and digital asset infrastructure. These are not separate battles—they are the same war, fought on two fronts.

What This Means for the Make Your Wallet Your Bank Thesis

The core argument of Make Your Wallet Your Bank is simple: you don’t need a bank to be your bank. You need rails, security, and sovereignty over your own money.

For years, the weakest link in that argument was the fiat on-ramp and off-ramp. How do you move from dollars to stablecoins and back—without touching the traditional banking system? The answer was always: you can’t, quite yet. You still needed a bank account to fund an exchange, and a bank account to receive the proceeds.

Kraken’s Fed master account doesn’t eliminate that dependency entirely overnight. But it fundamentally restructures the power dynamic. A consumer who uses Kraken Financial as their primary financial institution can now:

• Hold fiat in a full-reserve, Fedwire-connected institution

• Convert to stablecoins on the same platform

• Access DeFi yield and programmable finance

• Convert back to fiat

• Settle directly on sovereign payment rails

Without touching a single traditional bank.

As Kraken’s Co-CEO explicitly identified as a near-term architectural goal, atomic settlement between fiat and crypto is coming. When it does, the friction that has kept consumers tethered to legacy banking dissolves entirely.

The Closing Argument

This is not a story about crypto getting lucky or regulators going soft. This is the predictable outcome of a well-capitalized, well-regulated digital asset institution doing five years of unglamorous work—regulatory engagement, operational audits, and sustained credibility-building. Kraken earned this.

The banking lobby’s immediate response is the most telling data point in this story. You don’t mobilize JPMorgan, Bank of America, Wells Fargo, Goldman Sachs, and the community banking associations within hours of an announcement unless you are genuinely threatened by what just happened.

They are threatened. And they should be.

Because if a crypto exchange can become a Fedwire-connected financial institution—operating on a full-reserve basis with a security architecture that surpasses anything legacy banking offers — then the question for American consumers is no longer can I trust crypto with my money?

The question is: why am I still giving my money to a bank?

Stablecoin Rewards in the Market Structure Bill: What the Markup Text Allows—and What It Prohibits

As the Senate Banking Committee prepares to mark up the Digital Asset Market Clarity Act, one of the most closely scrutinized sections is Title IV, Section 404, which addresses rewards, yield, and compensation associated with payment stablecoins.

Although public debate has framed this issue as a renewed fight over stablecoin “interest,” the bill text itself reflects a narrower and more structured approach. Rather than reopening the GENIUS Act’s core prohibitions, the market structure bill largely codifies and operationalizes the existing distinction between prohibited interest and permitted activity-based incentives, while adding disclosure and marketing constraints. Baseline Rule: Yield for Passive Holding Is Prohibited

The bill adopts a clear baseline rule: no interest or yield may be paid solely for holding a payment stablecoin.

Section 404(b)(1) provides that a digital asset service provider may not pay “any form of interest or yield (whether in cash, tokens, or other consideration) solely in connection with the holding of a payment stablecoin.” This provision appears in Title IV, page 190, lines 5–9.

This language mirrors the GENIUS Act’s treatment of payment stablecoins and confirms that:

Payment stablecoins are not savings products.

Passive, balance-based yield programs are not permitted.

The bill does not authorize stablecoins to function as deposit substitutes paying interest.

The markup text therefore maintains continuity with existing stablecoin legislation rather than expanding yield-bearing functionality.

Explicit Carve-Out: Activity-Based Rewards Are Permitted

Immediately following the interest prohibition, the bill creates a structured exception for activity-based rewards and incentives.

Under Section 404(b)(2) (pages 190–191), the prohibition on interest does not apply to compensation tied to specific activities, including:

Transactions, payments, transfers, remittances, or settlement activity

(§404(b)(2)(A), p.190 lines 39–41)Use of wallets, accounts, platforms, applications, protocols, or networks

(§404(b)(2)(B), p.190 lines 41–42)Loyalty, promotional, subscription, or incentive programs

(§404(b)(2)(C), p.190 lines 43–44)Merchant acceptance, settlement, or acquiring activity, including rebates

(§404(b)(2)(D), p.190 lines 44–47)Providing liquidity or collateral

(§404(b)(2)(E), p.191 line 49)Governance, validation, staking, or other ecosystem participation

(§404(b)(2)(F), p.191 lines 49–51)

As drafted, the bill recognizes that not all compensation associated with stablecoins constitutes interest. Rewards tied to usage, participation, or infrastructure support are treated as permissible, provided they are not framed as yield on held balances.

Marketing and Representation Constraints

The bill pairs permissive treatment of activity-based rewards with explicit marketing restrictions.

Section 404(c) (pages 191–192) prohibits any person from marketing or describing stablecoin-related compensation in a manner that represents that:

The payment stablecoin is a deposit or is FDIC-insured

The compensation is paid by the stablecoin itself or its issuer

The compensation is risk-free or comparable to bank interest

The identity of the party paying the compensation is obscured

Material information necessary to prevent misleading impressions is omitted

These provisions are designed to prevent consumer confusion between:

bank deposits and payment stablecoins, and

interest-bearing accounts and activity-based incentive programs.

Disclosure Requirements for Permitted Rewards

Even where rewards are allowed, they are subject to a mandatory disclosure regime.

Under Section 404(d) (pages 192–193), the SEC and CFTC are directed to jointly promulgate rules requiring clear, plain-English disclosure of any compensation paid in connection with payment stablecoins. Required disclosures must identify:

The activity that earns the compensation

The party responsible for paying it

All material terms

That the payment stablecoin is not an investment product

That it is not a deposit and not FDIC-insured

Absent these disclosures, marketing of compensation tied to stablecoins is prohibited.

Treatment of Third-Party Reward Programs

The bill also addresses the allocation of responsibility between stablecoin issuers and downstream platforms.

Section 404(f)(2) (page 195, lines 25–30) provides that a permitted payment stablecoin issuer is not deemed to be paying interest or yield solely because a third party independently offers rewards or incentives related to the stablecoin, unless the issuer directs the program.

This provision separates issuer conduct from platform-level incentive design and clarifies that issuer compliance is not automatically affected by third-party reward programs.

Summary of Accepted vs. Prohibited Stablecoin Yield

Prohibited under the markup text

Interest or yield paid solely for holding a payment stablecoin

Marketing that frames rewards as deposit-like, risk-free, or issuer-paid interest

Compensation programs lacking required disclosures

Permitted under the markup text

Rewards tied to transactions, usage, or participation

Loyalty, rebate, and promotional programs

Incentives related to liquidity provision or ecosystem activity

Third-party reward programs not directed by issuers, subject to disclosure rules

Conclusion

As presented for markup, the Digital Asset Market Clarity Act does not expand stablecoin yield rights, nor does it eliminate stablecoin rewards. Instead, it formalizes a distinction already embedded in prior legislation: passive yield on stablecoin balances is prohibited, while activity-based incentives are permitted within a regulated framework.

The bill’s approach reflects a regulatory choice to constrain stablecoins as interest-bearing instruments while allowing them to function as competitive payment infrastructure, subject to disclosure and marketing controls. The markup debate, accordingly, centers less on whether rewards exist, and more on how narrowly or broadly the line between “interest” and “activity-based compensation” should be enforced going forward.

Coinbase’s Godfather Moment: A Perfectly Coordinated Strike on the 5 Pillars of Finance

Last night’s Coinbase system update wasn’t just another product launch. It was reminiscent of that scene in the The Godfather where on the day of his nephew's baptism, Michael Corleone executed a coordinated hit on the heads of the five major crime families.

Similar to what Michael Corleone did in that iconic scnene, last might Brian Armstrong delivered a simultaneous blow to the five pillars of finance--crypto, banking, payments, remittances, and global finance. And the implications are massive.

The “Everything App” Is No Longer a Concept, It's A Reality

With the relaunch of its platform, Coinbase effectively debuted an "everything app" for global finance, collapsing what were once separate industries into a single, vertically integrated system.

Users can now access, under one roof:

Prediction Markets

Stock Trading

Equity Perpetuals and Futures

DEX Integration for all major crypto assets — including every Solana meme token

BTC and ETH Lending

Global Payments and Money Remittance

An AI-powered Coinbase interface

Coinbase Business

A Branded Stablecoin Launchpad

Yes, each of these products already exists somewhere else. But, what’s new and disruptive about Coinbase's system update is that it offers all of these feature, natively, compliantly, and at scale.

From my perspective as a stablecoin regulatory and compliance consultant, Coinbase’s stablecoin offerings--including a branded stablecoin launch pad is particularly intriguing.

With the overhaul of Coinbase’s platform—including its custom branded stablecoin program and zero-fee global wallet-to-wallet stablecoin payments, Coinbase hasn’t just expanded products, it has expanded the addressable market for stablecoins worldwide.

Here’s what that means:

1. Branded Stablecoin Launchpad

Coinbase now allows brands to create their own custom stablecoins—tokens that carry their identity, loyalty, and utility wherever they circulate. These aren’t just tools for crypto insiders, they’re native monetary instruments that businesses can deploy for:

rewards and incentives

seamless customer payments

programmable commerce

cross-border value transfer

All backed by Coinbase’s infrastructure and liquidity.

This effectively gives brands direct access to in-brand monetary issuance in a way that was previously only possible for banks or sovereigns.

2. Zero-Fee Global Wallet-to-Wallet Payments

Coinbase’s new payment stack—rolled out globally with zero fees for in app wallet-to-wallet stablecoin transfers—removes one of the biggest friction points in global finance: costly settlement. Traditional rails charge fees, intermediaries slow settlement, and remittances can take days.

Now via Coinbase, stablecoins can move instantly and cheaply around the world, bypassing expensive legacy systems and opening huge demand from:

global consumers

merchants and ecommerce platforms

payroll and contractor payments

remittances and cross-border business flows

The Global Market Just Got Bigger

Stablecoins were already becoming a backbone of digital liquidity and cross-border settlement. Their use in payment systems has ballooned, with trillions of dollars flowing through stablecoin rails each year as fast, low-cost alternatives to traditional money movement.

Now, Coinbase has dramatically increased future demand by giving:

brands a way to issue their own stablecoins

consumers free, instant global transfers

merchants easier settlement and payment acceptance

This isn’t incremental expansion—it’s a step-function shift in the size and utility of the stablecoin economy.

But as Peter Parker learned in Spider-Man, “with great power comes great responsibility.” The same is true for brands looking to enter the loyalty and rewards stablecoin marketplace.

Here’s where the opportunity and the risk—really lies.

The U.S. GENIUS Act has finally provids a federal regulatory framework for payment stablecoins, defining how they can be issued, backed, and used across the financial system. That clarity is a watershed moment for the ecosystem, but it also means brands that issue and use stablecoins must navigate a strict compliance regime:

📍 Full reserve and backing requirements

📍 AML/KYC and consumer protection obligations

📍 Licensing and operational standards

📍 Ongoing reporting and regulatory engagement

Coinbase has taken the lead in deploying the technology—but deployment without compliance is a regulatory landmine.

That’s where I come in.

Your Bridge Between Innovation and Compliance

The demand Coinbase has just unlocked for branded stablecoins and zero-fee stablecoin payments is enormous. But brands, fintechs, and platforms now face a new reality:

Innovation must walk hand-in-hand with regulatory compliance under the GENIUS Act.

Workding with Stablecoin Solutions can help your brand:

✅ design and launch GENIUS Act-compliant stablecoins

✅ build payment flows that meet federal standards

✅ navigate licensing, AML/KYC, and treasury rulemaking

✅ avoid enforcement risk while maximizing market reach

This moment is bigger than a mere system upgrade—it’s a structural shift in how money moves.

Coinbase may have just lit the fuse for stablecoins to power commerce, remittances, payroll, and global settlement. Yet the responsibility to manage risk and comply with regulatory requirements rests squarely with each issuer and brand. The market is ready—but sustained adoption at scale depends on compliance. That is precisely where Stablecoin Solutions is positioned to add value.

Why Visa’s Stablecoin “Advisory” Isn’t a Neutral Guide

Visa recently announced a new Stablecoins Advisory Practice operated through its consulting arm, Visa Consulting & Analytics. The service is marketed as a way to help banks, fintechs, merchants, and other institutions understand stablecoin strategy, market fit, and implementation. It includes things like strategy development, use-case sizing, and support for integration. On the surface, this may look like valuable guidance — but there’s a structural conflict of interest that most buyers aren’t being told explicitly.

1. Visa Is Not a Neutral Advisor—It Has a Direct Commercial Stake Visa’s advisory practice isn’t a standalone boutique consultancy leveraged for impartial strategy exploration — it’s embedded within a payments network that already has commercial incentives tied to stablecoin deployment: Visa has built stablecoin settlement capabilities and payment rails that integrate with its existing global network, and these initiatives have already reached billions in annualized settlement volume. Visa’s ecosystem includes stablecoin-linked cards, settlement projects, and network incentives that benefit when institutions use Visa’s rails and services. That means every recommendation from this advisory arm inherently flows through the lens of: “How do we drive more volume and products onto Visa rails?” An advisor with a commercial stake in a specific outcome simply can’t be neutral—no matter how well-intentioned the consultants are individually.

2. Clients May Be Directed Toward Visa-Aligned Outcomes When an advisory practice is part of an organization that profits from the adoption of specific technologies or rails, two predictable dynamics emerge: A. Recommendations favor integration with the parent company’s products Visa’s consulting arm is structurally incentivized to recommend paths that position clients to leverage Visa’s payments infrastructure and stablecoin rails—because that increases Visa’s own revenue opportunities. This is not inherently wrong — but it is inherently non-neutral. For a family office or institutional treasury looking for independent strategic guidance, a recommendation that emerges from a company that sells related products is not the same as an unbiased assessment.

3. “Training” and Strategy Can Be Used to Shape Market Narratives Visa’s offering includes stablecoin training and market trend programs through Visa University. The fee for its basic virtual stablecoin course is $2,000.00. But this raises a core question: If the education is produced by an entity with a product and ecosystem to promote, can it truly be independent? Training that appears advisory may in practice introduce vendor-aligned framing—especially when the outcomes being discussed align with the advisor’s commercial path.

4. Visa’s Advisory Is Built on the Same Path It Profits From Visa’s advisory practice launches at the same time that: Visa’s stablecoin settlement business reports strong growth (e.g., $3.5 billion annualized volume). Visa continues to expand stablecoin–linked cards and payment products. This is not a neutral research institute recommending general best practices—it is a payments company selling strategy that aligns with its business model. For family offices making strategic decisions about stablecoin usage in treasury, payments, and international cost structures, that’s an important distinction.

5. Advisors With Skin in the Game Are Different from Independent Strategists When a family office engages an advisor, the three attributes that matter most are: Clarity Clear, candid assessments of risks and rewards, without product bias. Neutral exploration True strategic options — not routes that privilege a particular vendor. Decision support Insight that helps the client decide for themselves, not sell them a path. Visa’s Stablecoins Advisory Practice mixes consulting with embedded product incentives because: Visa benefits when more institutions adopt Visa-linked stablecoin rails Visa benefits if clients choose solutions that increase volume on its network Visa benefits from training that familiarizes clients with its ecosystem That’s not the same as impartial market guidance. If a consultant has an incentive to steer toward specific infrastructure or partners, that raises legitimate concerns about: whether the advice is aligned with true client interest whether alternative approaches were fully explored whether assessments of tradeoffs were even handed

6. What Truly Neutral Advisory Looks Like — and Why It Matters Neutral advisory should include: Independent evaluation of all relevant infrastructure options Clear disclosure of incentives or conflicts Head-to-head comparisons, not implied preferred vendor paths Frameworks that prioritize client outcomes over partner sales

At Stablecoin Solutions, we provide strategic, regulatory-aware guidance without selling infrastructure, products, or rails—meaning recommendations are shaped only by client outcomes, not by what benefits a payment network incumbent.

From Deposit Tokens to Stablecoins: A Real-World Illustration of the JPMorgan–Coinbase-Circle Flow

One of the most interesting developments in digital dollar settlement is the new interoperability between JPMorgan’s deposit token (JPMD) and Circle’s USDC through Coinbase’s Base network.

To understand why this matters—and why it fits squarely within the GENIUS Act’s regulatory boundaries—it helps to look at a concrete real-world example.

Let’s call the corporate Company X.

🚚 Scenario: Company X Needs to Pay an Overseas Supplier

Company X is a U.S. corporation that banks with JPMorgan. They keep a portion of their operating cash in a JPM corporate account, just like any major business. JPM gives them the option to “tokenize” a portion of that balance into JPMD, a bank deposit token that functions as an on-chain representation of a normal corporate bank deposit.

One day, Company X needs to pay a supplier overseas.

Here’s the critical detail:

The supplier wants to be paid in USDC, not through wires or SWIFT. They prefer USDC because settlement is instant, transparent, and far cheaper than the traditional banking rails—and because it can be converted into local currency (or used on-chain) with minimal friction.

This immediately creates a challenge for Company X: How do you convert a JPMorgan deposit (JPMD) into a GENIUS-ready stablecoin (USDC)?

That’s where the JPMorgan–Coinbase integration comes in.

🔄 Step-by-Step: How Company X Executes This Payment

1. Company X Tokenizes Part of Its JPM Balance

Company X converts $500,000 of its JPM account balance into JPMD.

This remains a JPMorgan IOU—it’s still a bank deposit, just represented as a token.

Importantly, JPMD is not a GENIUS Act stablecoin. It’s a fractional-reserve deposit token, only available to institutional clients.

2. Company X Moves JPMD to Base (Coinbase’s L2)

This is the innovation that matters.

Company X instructs JPMorgan:

“Move $500,000 in JPMD from the closed JPM network onto the Base blockchain.” JPM transfers the tokenized deposit onto Base, an environment where Company X can interact directly with USDC liquidity.

3. On Base, Company X Swaps JPMD → USDC

Once the JPMD tokens are on-chain, Company X uses Coinbase Institutional (or any approved liquidity provider) to convert:

$500,000 JPMD → $500,000 USDC

This swap happens on an open blockchain but with institutional-grade controls. Now Company X holds USDC, a fully reserved, GENIUS-Act-ready payment stablecoin.

4. Company X Sends USDC to the Supplier

With USDC in hand, Company X sends:

500,000 USDC → Supplier’s wallet

The transfer settles in seconds. The supplier immediately receives the payment—no SWIFT delays, no correspondent bank fees, no multi-day settlement risk.

5. The Supplier Converts or Uses USDC

The supplier can now:

Convert USDC into local currency

Use USDC to pay downstream vendors

Deploy USDC into on-chain treasury products

Move it to fintech banks or custodians

Swap it for other assets

In short, USDC becomes the universal settlement layer that bridges disparate financial systems.

💡 Why This Matters For Company X

- 24/7 settlement

- No SWIFT

- No wire delays

- Complete transparency

- Lower FX friction

- Immediate confirmation of receipt

💡 Why This Matters For the Supplier

- Instant payment